(toll free)

Avoid These 7 Costly Medicare Mistakes

This is the same guide I use in real client conversations. Learn the pitfalls — and how to avoid them

Why I Do This - A Promise to Memaw and Every Family

I got started in Medicare through the need to assist my Memaw. My mother passed when I was younger so Memaw became my responsibility. Some mistakes were made in her Medicare before I became old enough to help. Once I got involved, I had to fix some enrollment issues and I needed to make sure we didn’t spend precious dollars of her fixed Income on needless Co Pays and plan costs nor have limitations on her doctors or treatments.

The stakes are Critically High. If you miss an enrollment deadline, enroll in the wrong plan for you, or enroll in a plan too early or late, you could lose thousands of dollars, have penalties for life, lose and the freedom to see the doctor of your choice.

Medicare does a poor job of explaining how it all works and well-meaning friends, neighbors, and co-workers often give poor advice. Medicare is complex and constantly changing. That is why I do this. I wish we had a simple guide like this (and a Medicare pro like me to consult) when we started out. In the end, I saw Memaw through ups and downs and home nursing and feeding tube and ultimately to her passing in her sleep at age 93. Because I got her sorted out Medicare and her plans covered everything that ever came up. Helping Memaw live comfortably into old age was the best thing I ever did (before my son was born). This is dedicated to all the Memaw’s out there

The 7 Biggest Medicare Mistakes to Avoid

01

Missing Your Medicare Enrollment Window

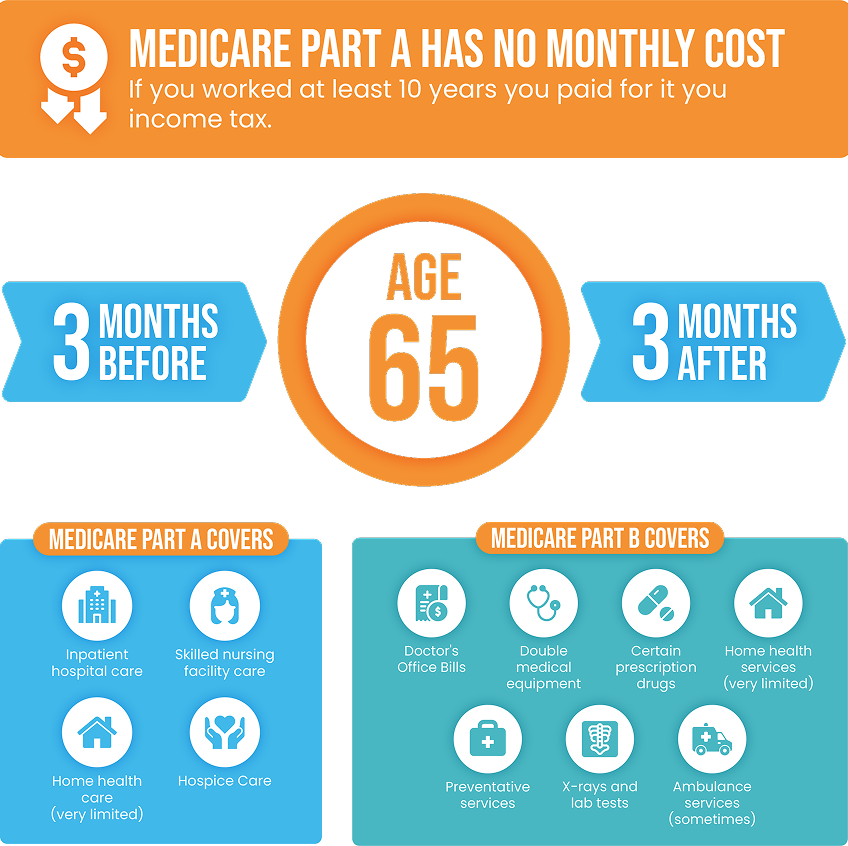

If you are getting money from the government in any form, for at least 4 months before your 65th birthday, then you are automatically enrolled In Medicare. You’ll get A and B automatically.

Part A (Hospital Insurance):

If you are not a social security beneficiary when you turn 65, you will need to manually enroll yourself in Medicare Part A and B during this 7 month window.

Part B (Medical Insurance):

It does have a monthly payment — it's $202.90/month taken directly from your Social Security. After that, Medicare pays 80% of your doctor bills and you pay 20% (uncapped).

02

Not Getting Part B / Getting It At Wrong Time

If you don’t get on Part B you get a Penalty. If you take Part B and didn’t need it (certain employer plans don’t require) then you pay $202.90/mo for no reason.

03

Part D - D Stands For (Drugs)

This one’s tricky. The government does not PROVIDE a Part D Prescription Drug Plan, but it does REQUIRE you obtain one. If you do not get one in your seven-month open enrollment window then you will begin to acquire a penalty. Once you do get a plan you will then have that penalty added to your monthly payment for Life.

Good news is- they are easy to get and plans are not expensive for most people. Send me your drug list and I'll tell you which are best options for you https://app.retireflo.com/chrisconnell

04

Not Applying For Low Income Subsidy

If you have limited income and resources to take care of the cost of your prescription drugs, Medicare has an “Extra Help” program to help ease the financial burden based on your income and assets.

The eligibility criteria for the subsidy are as follows for 2026

If you are single, your income must be below $23,475

If you are a married couple, your income must be below $31,725

05

Confusing Medicare Advantage with Medicare Supplement

So you have enrolled in Medicare (or will soon) and you’ll have what I call Government Issue Medicare, basic A AND B. And now you know you have these HOLES in Government issue Medicare. And here’s a quick breakdown again of those costs:

Part A deductible – $1,736 in hospital deductible every time hospitalized

Part A Co-Insurance – $434/day 61st day of hospitalization and $868 daily for lifetime reserve days. Your coverage is fully used up after the 150th day.

Part A- Skilled Nursing Facility Co-Insurance – $217 daily from the 21st to the 100th day of extended care services. After 100 days you pay 100%.

Medicare Part B Co-Insurance – 20% on expenses without a limit on what the 20% costs.

06

Doing Nothing

Analysis Paralysis is a real problem for some. Medicare is confusing and some people just get anxiety and then do nothing. BUT when a health issue arises those out-of-pocket costs and the lack of a Drug plan really mess them up. Don’t “Do Nothing”. Reach out to me and I’ll gently help guide you in the right direction. 800 850 1765

07

Not Reviewing Yor Plan Annually

The Medicare And You guidebook tells everyone they should have their plan reviewed every year. Advantage Plans in particular are constantly changing, networks changing. A very common (and sad) mistake is Advantage Plan customers will sit in an old stale plan when there were newer/better plans for them. I do a quick plan review for anyone who asks, no charge. Submit your drugs and doctors and I'll reply with your best Advantage Plan option https://app.retireflo.com/chrisconnell

Avoid These Traps and Choose A Plan With Confidence

These are just a few of the costly pitfalls I help my clients navigate. For a free, personalized review of your specific situation, book a no-pressure call with me today.

Or just Call me 229 740 6262, toll free 800 850 1765

Why Use Your Life Agency and Chris Connell to Help You

With years of experience and 600+ 5-star reviews, Chris Connell brings trusted, personalized Medicare guidance.

Experienced & Certified

Certified by all major carriers with years of real-world Medicare experience.

Local & Personal Support

No 800 numbers — talk directly with Chris whenever you need help.

600, 5-Star Reviews

Hundreds of seniors trust him — and the results speak for themselves

Advanced Comparison Tools

Easily compare the best plans and prices across top companies.

Your Medicare Journey, Simplified — With Trusted Support

Your Medicare journey doesn’t have to be confusing or stressful. With trusted support and clear guidance, we’re here to help you make confident decisions every step of the way — so you can focus on what matters most.

No spam. No robocalls. Just real help

I give Folks honest, personal help with Medicare + Life Insurance— so you can make a confident decision and avoid costly mistakes. Built on personal experience. Backed by 600+ 5-star reviews.

contact

We do not offer every plan available in your area. We only offer plans we feel are worth your time and money and have a good track record. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options

© 2026 Your Life Agency. All rights reserved.